|

|

|

|||

Department of Agriculture and Food Systems

|

||||

|

||||

|

|

|

|||

Department of Agriculture and Food Systems

|

||||

|

||||

|

|

Agribusiness Perspectives Papers 1997/98Paper 6/4 Putting The Family Back Into The Family FarmPaper 4 (of a series of 6 papers) Geoff Tually [Paper: 1 | 2 | 3 | 4 | 5 | 6 ] Every business operates within an ownership structure, eg., single proprietorship, partnership, trust, company (joint venture, not discussed here) or some combination. Each ownership structure will suit a range of farm family situations. The ownership structure is about who owns the business and its assets. This paper looks at the following three (3) aspects:

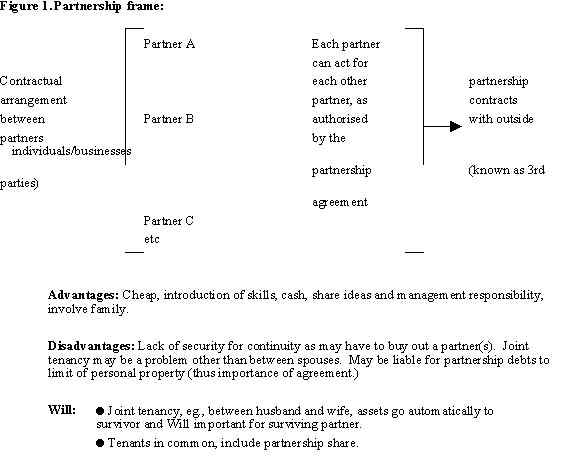

1. Selecting an appropriate ownership structureA basic understanding of ownership structure is vital for The basic framework. i) Single proprietorship. All business assets owned by one person. Advantage: cheap and easy to set up. Disadvantage: Ideas, cash may be limited. For a family situation would not allow family ownership. Will: Vital with a family situation, to be current. ii) Partnership. A simple contract between the parties involved consists of three (3) parts; a) Agreement: what members agree the partnership will do and extent of authority to act for each other. The membership and termination conditions (death or withdrawal of a member will terminate the partnership, which for capital gains tax will constitute a change in ownership of the business.) Agreement should be written, as oral agreements are difficult to remember or prove. b) Consideration: what each partner brings to the partnership, eg., cash, skills, machinery, loan of land, etc. The cash value of what you bring to the partnership may be the basis of partnership share, but may be negotiated on skill or loan of land or any other basis, eg. gifting. c) Intention to be legally bound to the agreement. (contracts willingly entered into will be upheld by the courts. Must be legally able to contract, ie. 18 years or necessary for their future).

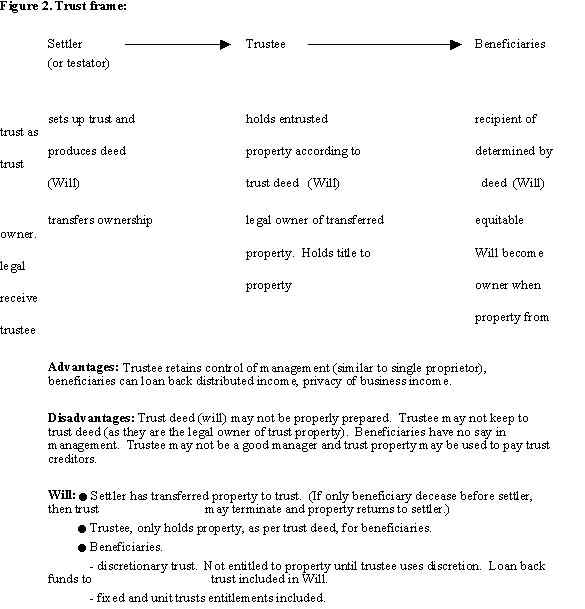

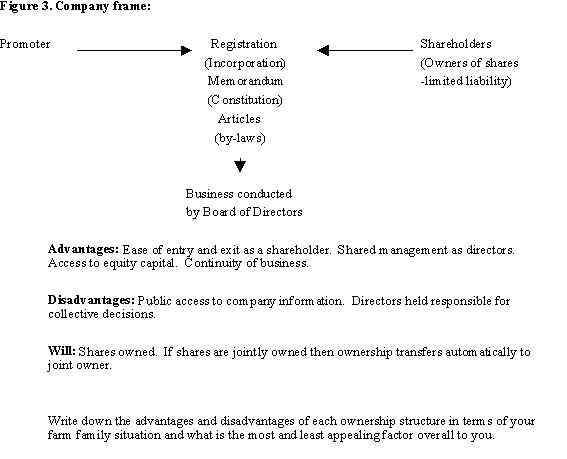

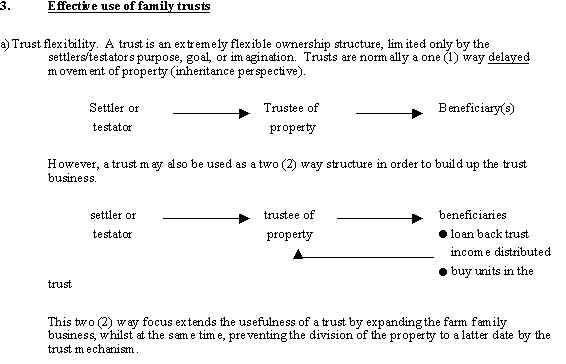

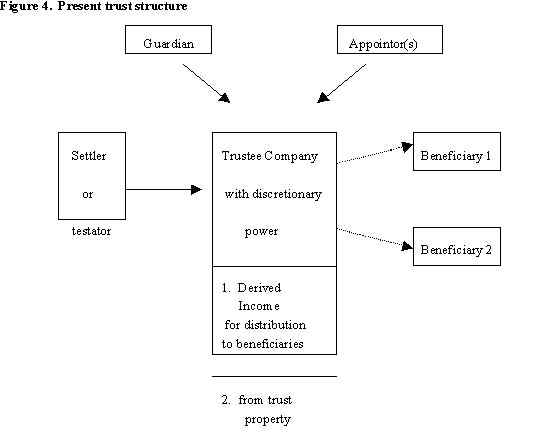

iii) Trusts A mechanism set up by a settler or testator (by Will), for transferring property (real and /or personal) to chosen beneficiaries at some time in the future, via a trustee. The trust deed provides the terms and conditions the settler or testator sets out for the operation of the trust. Must have property, deed and at least one beneficiary, for the trust to commence and continue.iv) Company. A company has same legal position as a person and is formed by incorporation under the Corporations law and may sue and be sued. The Corporations Law sets out how a company is formed, run and terminated. Shareholders provide equity capital (shares are personal property). Company owns the company assets. Shareholders are the owners of the company through their shares.

2. Changing from one ownership structure to another ownership structureChanges may occur due to:

a) Factors involved with voluntary change. Determining the reason for change. i) Present ownership structure - what it cannot do in terms of your/family goals, eg. son/daughter to join partnership (any change in the membership of a partnership terminates the partnership AND ownership of the business and thus subject to capital gains tax, if applicable). Reasons for change: ____________________________________________________________ ii. What you/family want the proposed ownership structure to do iii) Which ownership structure provides for your/family needs __________________________________ b) Factors that prevent a change in present ownership structure, eg., life tenancy, no agreement between membership of a partnership for a change, cost of stamp duty. Inhibition of present change _________________________________________________________ c) Alternative to a change in the present ownership structure - start another ownership structure, i.e, Joint venture, single proprietorship. Capital gains tax (C.G.T) will apply where the ownership of an asset changes (assets pre C.G.T will lose that status after a change) Suggestions:i) Parents own land, i.e., in an established partnership, and wish to involve children. Form a new partnership, trust of company to take over the business and lease land to businesses. Livestock (not subject to C.G.T) can be transferred to business when prices are low (ave value = market value), until then the breeding herd leased to business. ii) Sons/daughters commence off or on farm businesses and lease/rent farm family assets, ie., contract harvesting, provide record keeping service to other farm families.

The Guardian and Appointors (figure 4) play a significant role in preventing a trust from termination, i.e., through divorce. The trustee has generally been the controller of trust property and the Family Law Court has divided farm property held by a trust where the trustee has been one of the parties to a divorce. The Guardian and especially the Appointor, being separate to the trustee, now in reality control the trustee and protect trust property using a company as the trustee adds security.

c) Unit trust. This allows for all farm family members to buy in to increase the equity in the business and at the same time allows the unit holders to sell their units to other family members. Units are personal property and can be used as property for another trust, ie. son/daughter may buy units in farm family business and use their units as the property for their own family trust for distributing the income from the Units. |

|

Contact the University : Disclaimer & Copyright : Privacy : Accessibility |

|

Date Created: 04 June 2005 |

The University of Melbourne ABN: 84 002 705 224

|